Update #3 - August 20, 2024

HelloFresh, Titanium Transportation and Gold Royalty

In this post I will dive into the recent developments, news, outlook and other relevant information of the following companies:

HelloFresh $HFG

Titanium Transportation $TTNM

Gold Royalty GROY 0.00%↑

HelloFresh

You can find the original thesis for HelloFresh here:

Repurchase Program

Since the thesis writeup HelloFresh started repurchasing shares more aggressively, buying back first €1.5M and then €2M per week in shares. Since their last earnings report on March 8th, they have repurchased 2.93% with a ramp up that started in July. They are now purchasing €2M per week for about 0.2% of the company, which annualized is 10% per year.

Q2 Results and Conference Call

HelloFresh reported a growth of 0.9% in constant currency revenues with an EBITDA of €146M, a margin of 7.5%, €19M over consensus expectations. The meal kits business saw a decline of 9.3% YoY in revenues, continuing its downward trend which was augmented by the marketing budget shifting to RTE and the focus on customers with a longer LTV (LifeTime Value). This caused the absolute number of clients to decrease and the AOV (Average Order Value) to increase. Meal kit margins were 12.2% for the quarter, well over the guided 10%. On the RTE side, revenues grew 47% YoY and margins remained flat at the guided 4% level. Procurement and cooking expenses were up as a percentage of revenue, increasing 300 basis points YoY because of the higher share of RTE which has higher costs. However, procurement expenses for the North America RTE are down 170 basis points QoQ as efficiencies start to take effect.

As a result of the shift towards higher LTV clients, HelloFresh is now reducing their footprint, which led to impairments of €44.7M in H1, while management commented that retention levels were ‘robust’. Marketing spend was lower than in Q1, as is usual given the seasonality of the marketing expenses. Q3 marketing costs will be similar to Q1 levels while Q4 will be like Q2.

Regarding financing and liquidity, the company entered into a €190M term loan facility that will allow them to refinance their bonds, which matured on May 2025. There originally €175M worth of bonds and €23M have been repurchased so far. HelloFresh also announced a reduction in capex of €40M, leaving capex for the year at €240M instead of €280M. The capex guidance for 2025 and beyond remained at €200M. Cash from operations for H1 was €146.9M, with capex of €96M, leaving FCF at €50.9M. Net cash at the end of the quarter was €233M, an improvement of €26M, which supports the buyback program.

When it comes to guidance, management commented that they maintained the guidance they gave a few months ago, expecting an improvement in EBITDA in the second half of the year.

There were some nice comments on the Q2 letter to shareholders, which I do recommend reading. Among them I would highlight this one: “With the benefit of hindsight, we acknowledge today that we were too optimistic at extrapolating future new customer volumes from a near pandemic baseline and ultimately struggled to achieve the growth we aimed for”. It is also worth mentioning this comment about RTE: “We are confident that the RTE product category will not just be a growth story but also one of margin expansion in the coming years”. My personal opinion is that the letter reflected well the current situation of the business and the humility of the management team in recognizing their mistakes while outlining the goals for the next few years.

Titanium Transportation

You can find the original thesis for Titanium Transportation here:

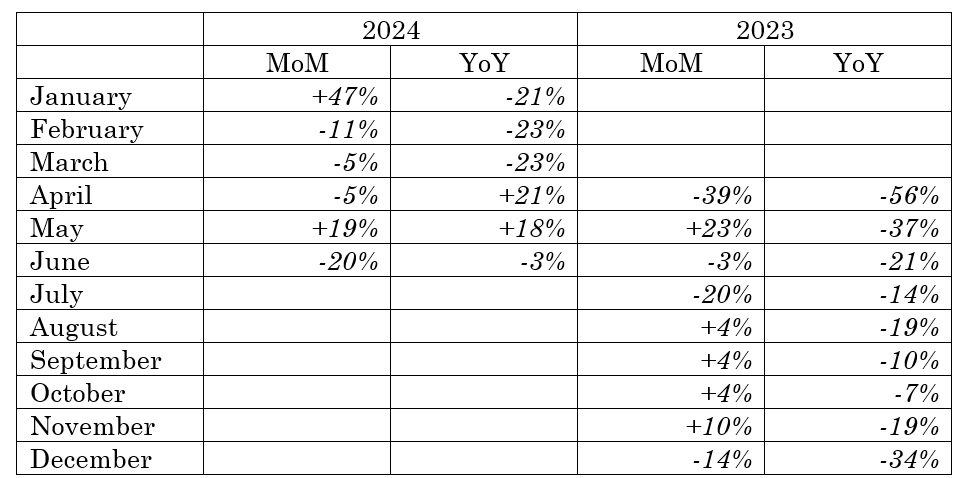

LoadLink Load Index

Loadlink provides an index estimating the number of loads in the market, which I forgot to include in the thesis. The index can be found in the following link:

The numbers for the last 12 months are:

Q2 Results and Conference Call

Titanium reported a 14.7% increase in revenues for the quarter, largely due to the acquisition of Crane, which was completed in July last year. Truck transportation grew 20.7% while margins were impacted by the integration of Crane, which is taking more time to complete given the market conditions, and pricing pressure also because of the market conditions. The segment made an operating loss of $0.6M. Management said that “contract pricing came under similar pressure to transactional pricing, falling to nearly unsustainable levels”. Truck transportation pricing went down 6% YoY. It is also important to note that revenues grew $16M for trucking, $13.7M of which were from Crane, so the truck segment also grew $2.3M organically, or 4.6%. For the logistics side of the business, revenues grew 6.6% and operating income was $3.1M, a margin of 6.2%. Again, margins were impacted by the market conditions. EBITDA margins were at approximately 10% both for Q2 and YTD.

Nevertheless, volumes grew 24% in the trucking segment and 22% for logistics. At the end of the day, what Titanium can control are volumes and margins, whit the price being set by the industry. They have mentioned several times now that the market is approaching an unsustainable level and at some point, it must reverse, and prices should stabilize if not start rising again. It is in this moment when the gain in volumes seen in the last couple of years will be reflected in the financial statements. If prices start rising again, revenues will grow much faster than volumes, but if they only stabilize revenues will grow at a nice pace, given the current volume growth.

Regarding the recovery of the industry, management commented: “Indications of an improved balance between freight demand and industry capacity are also, somewhat hesitantly, starting to emerge. We are anticipating freight market conditions to improve in the first half of 2025”. They previously said that they expected the market to improve in H2 2024, so they pushed it back 6 months. As a result, they also adjusted the guidance to $440 to $460M and EBITDA margins of 8% to 10%. They also expect the margins to be affected by the acquisition of Crane for a few more quarters, which they didn’t before. This is the second time they adjust the guidance in 2024. The previous guided numbers were:

Net debt was reduced by $20M to $171M while annualized H1 EBITDA is $40M, which leaves the Net Debt to EBITDA ratio at a very high x4.3. It is likely that they will end the year at x4, since they will repay some debt in H2. Titanium has $63.9M in liquidity resources available under their current facilities.

Titanium’s management has been quite active in mitigating the effects of such negative market conditions, by selling redundant or unused assets, ceasing operations in areas with ‘heavily deteriorated market conditions’, and identifying further synergies between the trucking and logistics segments. They will also sell $5M worth of aged equipment (according to Titanium’s standards).

At this point, the situation seems quite dramatic. Nevertheless, I think that it not as dramatic. Volumes have grown at a very good rate and at some point, prices will recover. Meanwhile, Titanium is focused on completing the integration of Crane, reducing net debt, selling unused or redundant assets and optimizing their operations. Furthermore, they have more than enough liquidity, even for a further small to medium acquisition. I think the pressure is just temporary and will last only a few more quarters, probably 2 or 3. But the truth is that Titanium is not doing so bad and the proof of this is in the FCF, which was $11.2M for the quarter. The YTD figures are $16.9M, which annualized is $33.8M, and the company is trading for roughly $90M. Right now it is a very leveraged company, but if we look at 2025 year-end numbers, not so much. Take $170M in net debt, with annual repayments of $40M, it will be at $110M and when EBITDA recovers to 2023 levels (just absolute EBITDA, not margins), which was about $50M, Titanium quickly deleverages to x2.2. The current leverage is more a result of a depressed EBITDA rather than actual high debt levels.

It is now clear that what I had predicted for 2024 will not hold true as the trucking and logistics market are quite tough right now. Nevertheless, I believe Titanium continues to operate well, increasing the volumes in both segments, and I think it is a matter of time before the market recovers and Titanium goes back to growing their revenues and profits like they have done for many years. Regarding my expected numbers, I think that they can still hold true if you push them back a year or maybe a year and a half into the future. Again, the prices will recover and with them Titanium will recover their sales growth, margins and profitability.

Gold Royalty

You can find the original thesis for Gold Royalty here:

Q2 Results and Conference Call

Gold Royalty reported revenues of $2.2M or 947 GEOs while costs were down 9% for the comparable period, continuing the trend of positive cash from operations. For the first half of 2024 the revenue was $6.4M or 2,967 GEOs, which is already more revenue than in 2023.

There currently are 7 cash flowing assets, which provided the following revenue:

Regarding the main assets and their development stage, the Canadian Malartic royalty entered commercial production earlier this year and is expected to provide 2,400 GEOs for 2024. Côte Gold achieved commercial production in August at 60% production capacity, with the aim of reaching 90% by year end. They also mentioned that Côte will be in the lower end of the guidance, so about 1,650 GEOs. Vares is expected to “meaningfully ramp up” in Q3 and Q4, achieving commercial production in the last quarter of 2024. Furthermore, Adriatic Metals, the operator of Vares, is studying increasing the production capacity from 500,000 to 1,300,000 tons per year. Borborema is in construction with about 40% completed, with the expected start of production being sometime in Q1 2025. When construction is fully completed, the pre-production payments from that royalty will cease and the 2% NSR will kick in. This will mean that Gold Royalty will lose 1,000 GEOs per year and receive the actual royalty, which is expected to be less than 1,000 GEOs for the first year. There is also some upside potential for Vares, Canadian Malarctic and Borborema, since not all of the resources of the mine are incorporated into the mine plan, allowing for either a longer mine life or a higher production capacity. Finally, Cozamin is an established mine providing about $1M per year. All in all, main assets are in a ramp-up phase and the next few years, especially 2025, should be quite good since many assets get to commercial production. They also mentioned that the consensus figure for GR’s revenue is 30,000 GEOs by 2030, which at the current gold price ($2,500/oz) is $75M.

Market Concerns about GROY

About a year ago, the market had concerns about Gold Royalty’s near term cash flows as they were not expected to be positive until a few years later. The management team addressed these concerns by acquiring cash flowing royalties like Cozamin, Vares or Borborema. Now the market is worried about further dilution to shareholders, since some of these acquisitions were paid via issuing shares or convertible bonds.

Historically they have said that they would only issue shares if they had “a clear use of proceeds” that was accretive to shareholders on a per-share basis. I believe that has been the case, however, they may have diluted a bit too much in trying to solve the previous market concerns, cash flows. So far management has only issued shares to purchase accretive assets on a per-share basis, at least in my opinion, which is a good thing even if it is neither accretive nor value destructive in per share terms, since it helps GROY gain scale and therefore a better valuation multiple. Nevertheless, I expect that management will reduce significantly the issuance of new shares or stop it completely.

Disclaimer

This article is not a financial advice. I am not a financial analyst. If you are going to invest do it under your own risk and after doing the appropriate due diligence.