HelloFresh ($HFG) - Part 2

Growth Strategy, Projections, Insiders, Risks, Competitors, Valuation and Summary.

This is the second part of the HelloFresh thesis, in which I will explore the company’s growth strategy, the projections for the next quarters and years, insiders and shareholders, risks, competitors, valuation and summary of the thesis.

You can read the first part of the HelloFresh thesis here:

Note: this is the original thesis. You can access updates and new news about the company in the “Updates” section or at the end of this thesis, where you will find a link to all the updates.

Growth Strategy

Targets

A few years ago, HelloFresh outlined their goals for 2025. They targeted €10B in sales and €1B in adjusted EBITDA, with about 29% contribution margins. On March 8th, 2024 they said they would not be able to reach those goals by 2025, which should have been clear by then. Nevertheless, this caused a 40% decline in the stock.

The company also provided guidance for 2024. They expect to grow their revenue 2% to 8% and an adjusted EBITDA of €350M to €400M. Factor is expected to grow 50% from €1.4B to €2.1B in sales. The full guidance means that revenues will grow about €380M while Factor’s sales are set to increase €650M, meaning that the meal kits and other verticals are expected to lose €320M in revenue, a decline of about 5.2%.

2023 Strategy and Growth Plan

For 2023 the company focused more on profitability and finishing the last growth phase in order to adjust the cost base to the revenue level. This is expected to continue in 2024 and possibly also into 2025. This is why they have stated that “2024 will be a relatively complex transition year for HelloFresh”.

Focusing on the meal kit segment, for advanced markets they want to further improve unit economics, improve customer proposition by adding new recipes and customization, and capture reactivation opportunity. Regarding this last point, when trying to reacquire inactive clients, that is those who cancelled their subscription or paused it for a long period of time, they have twice or thrice the conversion rate versus unacquired customers and also better retention levels versus newly acquired clients. For underpenetrated markets they want to get the ROI levels up to those of developed markets and elevate penetration levels by further implementing the meal kit playbook and improving the customer proposition by adding delivery days, market presence, number of recipes and brand awareness to levels of the advanced markets.

For the RTE segment they want to keep implementing the meal kit playbook, invest in new production facilities, as was mentioned in the capex section, and start the internationalization of Factor into Europe, which started at the end of 2023.

Regarding the customer proposition, they want to keep adding recipes and improve customer proposition, as was previously mentioned. In 2024 they are targeting expansion of physical product offering, improve marketing efficiency and switch from financial incentives to product incentives for new customers. For the distribution and fulfilment centers they want to finalize the remaining capacity expansion projects, standardize projects and optimizing the distribution centers, network structure and design.

Due to the shift in the market conditions, they have stated that “with more moderate growth expectations, we will target faster expansion of meal kit earnings than top-line in the coming years”.

Focusing on mid-term goals, they want to increase penetration in all markets, even the developed ones and gradually enter new geographies and launch new verticals. They provide this slide which shows the potential additional market that they could capture in the coming years. It is important to note that they consider mid term to be anywhere from 3 to 5 years.

Regarding mid-term margins they target 10% for both the meal kits and the RTE business lines. The meal kits are close, with current margins of 9%, but the RTE margins are still at 4%. However, they state that Factor has a “clear path toward >10% adjusted EBITDA margins”, as gross margins improve as a result of volumes doubling, and marketing expenses going down to the same level as the meal kits, plus a maturing customer base for RTE meals. For the group’s margins they have said that “we see an opportunity to improve margins by up to 3% through procurement levers and improved DC productivity”, 100 basis points from procurement efficiencies and 200 basis points from fulfillment and distribution center improvements.

Finally, a couple of notes. For marketing expenses, they expect them to be 15% to 16% of revenues in the mid term. When looking at marketing decisions, they look at the lifetime value (LTV) of the client versus the customer acquisition cost of that client (CAC). They typically get payback on their investment in about 6 months. For 2024, they are changing their marketing strategy to target fewer clients but focus on those that have a higher LTV, while aiming to maintain the CAC. This translates into improved efficiency in their marketing spend and higher-value clients. The other note is on their criteria for new opportunities. They must be $500M+ of revenue, positive marketing ROI in 3 years, positive EBITDA contribution in 5 years and it must be the best use of capital at group level. If the expansion is into a new geography but not into a new business, they have said that the EBITDA breakeven is also 5 years, but the peak low EBITDA is 3 years after the launch as the business ramps up.

Projections for the Next Quarters and Years

For 2024, as was stated before, the guidance was 2% to 8% revenue growth and €350M to €400M. This leaves adjusted EBITDA margins at 4.7%. HelloFresh also expects sequential improvement in meal kits revenue on or after Q2 2024 and costs reductions starting in 2024 whose benefits will be visible in 2025.

For 2024 margins are expected to be lower because of two key factors, RTE expansion in North America and the transition into new fulfilment centers for meal kits. The meal kits margin is expected to decline from 9% to 8% because of that transition into the new fulfilment centers while maintaining the old ones until the new ones are fully operational. That results in duplicated costs for about 12 months. For the RTE business, the improvement in margins resulting from the implementation of the meal kit playbook is expected to be offset with the costs from the ramp-up of the production capabilities. Regarding the margin outlook, they have stated that: “We’re maintaining adjusted EBITDA margins in many of our day 1 markets significantly higher than 10% today, but off of the pandemic highs of greater than 15%”. In a longer-term perspective, they have said that they could reach 10% in both meal kits and RTE in 3 to 5 years.

Insiders & Shareholders

Insider Ownership & Salaries

Dominik Richter is the Group CEO & Founder of HelloFresh, and he has been in the position since 2011. Thomas Griesel is also a Founder of HelloFresh, and he has been the CEO of the International markets (outside of the US). He is also the CEO of TWG Ventures, a company through which he owns his HelloFresh shares. Finally, Christian Gaertner has been the Group CFO since 2015. He was previously an analyst at Deutsche Bank for 2 years, and later a managing director in Goldman Sachs for 12 years and then at Bank of America for 4 years.

Regarding Insider Ownership, Richter owns 4.12% of HelloFresh and Griesel owns 1.71%. Furthermore, there is a binding commitment for all members of the Management Board to own at least x1 their gross fixed salary in HelloFresh shares, or about two times their net fixed salary. Insiders as a whole own 7% of HelloFresh.

Finally, focusing on salaries, the compensation structure has changed recently. The maximum compensation is now limited to €14M for the CEOs (Dominik Richter and Thomas Griesel) and €11M for the other board members.

Dividends & Share Repurchases

HelloFresh has never paid a dividend, but they have done share repurchases. The first one was in 2022 and they repurchased 2.2M shares or 1.17% for a total of €125M in the span of a month, 50% of the approved amount for the buyback. They approved another buyback program in October 2023 for a maximum of €150M. As of June 3rd, they have repurchased 5.5M shares or 2.91% for €65.5M. Year to date, 3.641.592 shares have been repurchased. Net shares at Dec 31st 2023 were 171.110.806.

It seems that they have since slowed down the buyback program, however HelloFresh has a net cash position of €207M so they can keep repurchasing shares. The remaining balance on the buyback program is €80M, which at the current price (5.65€) is the equivalent of 8.27% of the company. Nevertheless, I believe that given the current net cash position and the depressed share value, they should be repurchasing much more.

Finally, it is also important to note that some management members have been buying shares. Insiders purchased a lot of shares in 2022, very few in 2023 and they have started purchasing more shares again in 2024. The 2024 share purchases by insiders were:

The total amount of insider purchases was €1.3M.

Risks

In my view, HelloFresh faces the following risks:

Margin compression: if they can’t go back to the unit economics previous to those achieved in the covid years, margins will be impacted, and it is possible that they don’t get to the 10% target. Also, the necessary level of marketing costs could be higher than what they have anticipated.

Operational Execution: any problems in migrating their fulfilment centers could cause extra costs and may even result in losing some clients.

Change of Management: the current management team founded HelloFresh, turned it into the best company in the industry, made it the only profitable one and identifying new business lines, like that of the RTE business, and applying the same tactics used to dominate the meal kit industry. Although they benefited in part from the early mover advantage, many other companies were early players too, but HelloFresh was the only one to achieve profitability and dominate the industry.

Competitors

As I have just stated, HelloFresh enjoys significant competitive advantages that are visible in almost every aspect of their operations. They are the only non-niche profitable company in the industry, and they clearly dominate the market. It is very hard to disrupt HelloFresh’s business and none of their competitors have been able to achieve profitability, much less threaten HelloFresh. The main competitors are Dinnerly, Blue Apron, Home Chef and Plated for the meal kits and Fresh N Lean, Cookunity and Bistro MD for the RTE business, among others.

U.S. meal-kit rival Blue Apron was bought by startup Wonder Group for $103 million last year after warning revenue and customer numbers would fall in 2023. It was worth $1.9 billion when it was listed in 2017. They are HelloFresh’s biggest competitor.

Valuation

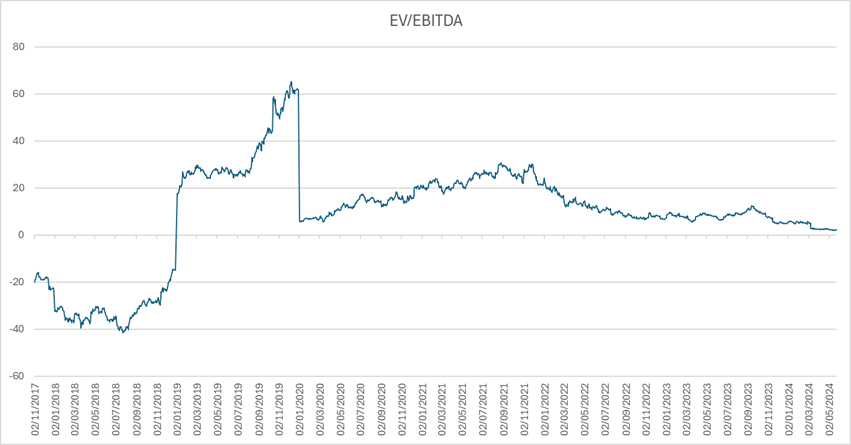

I think that in order to value HelloFresh the best multiple to use is EV/EBITDA because of the nature of the industry and how difficult it is, especially for competitors to achieve positive earnings or free cash flow. The evolution of HelloFresh’s valuation using EV/EBITDA (adjusted EBITDA) looks like this:

The 2017 to 2019 period is irrelevant since for some time HelloFresh had negative EBITDA and for 2019 the EBITDA was quite low and the multiple in that year is not useful to calculate the valuation of the company, since it was high due to the very attractive growth prospects of HelloFresh. Without accounting for those years, the EV/EBITDA looks like this:

The average multiple since 2020 has been x13.15 and for 2020 to 2022, when growth was expected to be higher than what was expected for 2023, the average multiple was x16.05.

For the valuation of HelloFresh, I have estimated three scenarios:

Optimistic: meal kits revenues decline in 2024 and 2025 and return to organic growth in the next years while margins gradually rise to 10%. For RTE, growth stays high although it slows down progressively while margins gradually rise to 8.5%, getting closer to those of the meal kits vertical. A fair value is considered to be at x12 EV/EBITDA. The price target for 2026 is 40€ and 60€ for 2028. This may seem too high but I think it is reasonable if the margins improved as assumed. Keep in mind that this is the optimistic scenario.

Medium: meal kits decline for 2024 what they declined in the first quarter and take more to stabilize, which they do at a level 5% lower than the current revenue. Meal kit margins improve but slower than what they do in the optimistic case. Similarly, RTE grows slower, and margins improve slower than in the optimistic case. The EV/EBITDA multiple is at x9. The price target for 2026 is 22€ and 27€ for 2028.

Pessimistic: meal kit revenues stabilize at a lower level, 15% lower than the current sales, while margins recover to 8.5% gradually. RTE growth significantly slows down while margins improve slightly but nowhere near what management said that they could be at. Corporate costs also increase significantly. A fair value of this scenario is set at x6 EV/EBITDA. The price target for 2026 is 12€ and 13€ for 2028.

Summary

All in all, I think that HelloFresh is an interesting opportunity given its significant competitive advantage, growth expectations, margin expansion and depressed valuation. If they can pull through the current challenges and return to a growth path in the future, the revaluation of the stock is quite compelling, especially given that its market cap is €946.2M with €207M in net cash, a valuation of x2 EV/EBITDA based on the midpoint guidance for 2024.

Disclaimer

This article is not a financial advice. I am not a financial analyst. If you are going to invest do it under your own risk and after doing the appropriate due diligence.

Updates

In this section you can find the most relevant news and updates from the company since the thesis was published. They are arranged in chronological order: