Valeura Energy - $VLE

A Very Interesting Opportunity in Oil & Gas

The thesis was originally written on January 2025, but it was published later in February after the reserves report. The information on the reserves report is at the end of this post.

You can read the thesis in Spanish here:

Note: this is the original thesis. You can access updates and new news about the company in the “Updates” section or at the end of this thesis, where you will find a link to all the updates.

Note: the company is Canadian but its financial statements are in USD and they use USD as the base currency. Therefore, throughout this report dollars will mean USD, while Canadian dollars will be explicitly stated.

Note: All production numbers are Valeura’s share of ownership, not total production.

History and Business Model

Business Model

Valeura Enery is a Canadian oil and gas company operating in Thailand. It is focused on petroleum production in the Gulf of Thailand, where Valeura is the second largest operator. The company also holds a license for a gas reservoir in the Thace Basin in Turkey. That asset is not being operated currently.

The company extracts oil through its oil rigs, which the company calls ‘offshore production units’. They have fixed and mobile oil rigs. From there, the oil travels from the rigs through a pipeline to the Floating Storage and Offloading vessel (“FSO”), which can be leased or company-owned. Those vessels are later emptied by a bigger vessel that picks up the oil when Valeura sells it.

Since Valeura has to hold the oil in the FSOs until they are almost full, at which point they sell the oil, they sell high volumes of oil at a specific price. Due to the timing of the sales, the realized price of their oil can vary slightly from the average oil price for the quarter, say ±$3/bbl. For the same reason inventories can suffer big changes from quarter to quarter.

History

The founders of Valeura had previously founded and later sold Verenex Energy, a company focused on Libya. They used the proceeds of that sale to create Northern Hunter. Valeura Energy was formed as a result of a merger between PanWestern Energy and Northern Hunter Energy in September 2010. They were then listed in the TSXV and then upgraded to the TSX in June 2011.

During the 2010s, the company focused on gas deposits in Turkey, mainly in the Thrace Basin. During these years, it generated between $14M and $25M in revenue.

In August 2020 the company decided to implement a clear strategy to add value for shareholders via M&A, with the goal of enhancing cash flows in the near/mid-term. Subsequently, they sold their gas assets in Turkey for $15.5M, with additional upside via royalties of $1.5M to $2.5M until 2025.

In April 2022, Valeura acquired two assets in the Gulf of Thailand: the Wassana oil field (89% share and near-term production) and the Rossukon oil field (43% share and near/mid-term production). In December 2022, Valeura acquired the Jasmine oil field (100% share), the Nong Yao oil field (90% share) and the Manora oil field (70% share).

At the time of the acquisitions, the CEO stated: “The company believes the Gulf of Thailand acquisitions establish a platform for re-investment of cash flows into additional growth opportunities”.

Additionally, in April 2023, Valeura acquired the remaining share of the Wassana oil field and sold their stake in Rossukon.

Transformational Acquisitions - Details

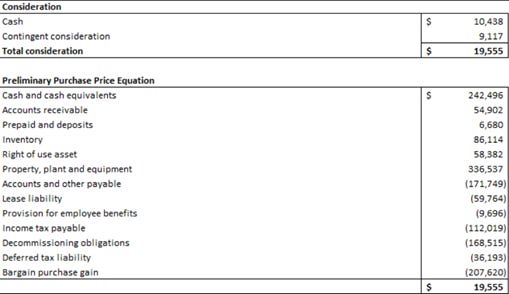

After the sale of most of the Turkish assets the company started looking for accretive acquisitions. They acquired two companies in Thailand, KrisEnergy and Mubadala. With the acquisition of KrisEnergy the company obtained a stake in two oil fields: Wassana (89% interest) and Rossukon (43% interest). They paid $3.1M plus another $7M in contingent consideration. At the time of the acquisition they expected approximately $9M in net cash flows per quarter (at $100/bbl, the oil price at the time). After the reserves were expanded in the middle of the acquisition, the total consideration was increased to $19.3M. When purchased, the NPV of those assets was $59.3M (using a 10% discount rate). They later sold their stake in Rossukon and purchased the remaining interest in Wassana, as explained below in the assets section.

The second acquisition was that of Mubadala, through which they obtained a 100% interest in the Jasmine oil field, a 70% interest in the Manora oil field and a 90% interest in the Nong Yao oil field. The assets produced 21,200 bbls/d and had reserves of 24.1M bbls for which they paid $10.4M with contingent consideration of up to $50M. Plus they had to pay the remaining taxes of $113.2M and net payables (receivables – payables) of $116.85M. At the time of the acquisition, Mubadala had $242.5M in cash. All in all, and including contingent consideration, Valeura paid $48M maximum. Here is the balance sheet of Mubadala when it was acquired and the final purchase price:

Both acquisitions turned out to be highly accretive for shareholders and were done without any share dilution. Particularly, the Nong Yao field is very profitable with operating costs of $22/bbl, which later fell below $15/bbl with Valeura as the operator. With just the Mubadala acquisition they expected to generate about $30M a month.

The acquisitions were made under a Special Purpose Vehicle (SPV), of which Valeura owned 85%, with the rest being the property of key personnel for the Thailand assets. Most of them had worked for Mubadala. Valeura later acquired the rest of the SPV in exchange for 9.5M Valeura shares, and the key personnel is now working for Valeura.

SouthEast Asia and Thailand Markets

Regarding the oil market, there is not much that the company can do to mitigate the risks other than reducing their operating costs. They can’t control the oil price but it affects Valeura’s profitability significantly. Currently the oil price is about $80/bbl. Regarding the southeast Asia region and Thailand in particular, Valeura is the second largest oil producer in Thailand and a regional consolidator with “low competition for their target size”. The oil and gas production has been declining in past years and demand is growing. The production in Thailand is about 150,000 bbls/d and consumption is 1,200,000 bbls/d. Furthermore, there is a reduced number of operators and governments are supportive and seeking proven operators. Additionally, for many of the assets, there has been very little exploration if any, which leaves potential for expansion of reserves.

Focusing on the regulatory environment, Thailand has a special tax policy for oil companies, called Thai I and Thai III. Under Thai I, the government takes a 12.5% royalty and a 50% corporate tax for oil sales. Under Thai III, the government takes from 5% to 15% in royalties and a 50% corporate tax for oil sales, plus a progressive tax from 0% to 75% on “windfall profits”, also called ‘Special Remuneration Benefit (SRB). (See Annex). Also, there is a 15% tax on any money leaving Thailand.

Portfolio of Assets

The assets that Valeura has are the following: equipment (FSOs, MOPUs, etc.), Jasmine, Wassana, Nong Yao, Manora, Rossukon royalty and the Thrace Basin project.

Equipment (MOPU and FSO)

Valeura acquired a MOPU (“Mobile Offshore Production Units” - aka mobile oil rig) from Nora Energy for a total of $9.2M. By owning the MOPU instead of leasing it the company reduces operating costs. At the time of the purchase, the MOPU needed to be re-certified for it to be operational. It was certified and is now operating in the Wassana field.

Additionally, Valeura also owns a FSO that is currently operating in Nong Yao. It has a capacity of 20,000 bbls/d and it was purchased for $19M. It allows for cheaper operations in Nong Yao.

Jasmine (License B5/27)

Jasmine was acquired through the Mubadala acquisition and it is the only field operated under the Thai I conditions (12.5% royalty and 50% tax rate). Valeura holds a 100% interest with production of 8,000 bbls/d. The oil from Jasmine is typically sold at a $2/bbl discount to the brent price, after which the company pays the 12.5% Thai I royalty and a further 4.5% royalty to a private counterpart. The opex for the field is about $30/bbl. For this field there are 6 facilities which pump their oil to a leased FSO, as can be seen in the picture below.

When it comes to exploration, Jasmine has proved to be a very fruitful field, with initial reserves (in 2005) of 7M bbls with additions of 95M bbls so far. 92M have been produced with the latest number for the 2P reserves being 10.4M bbls, which is 3.6 years of production, reaching the current economic life of the field of 2027. However, Valeura intends to keep exploring the field with 13 wells planned for 2025 that aim to expand the economic life to 2032, when the licence expires. 7 of those wells (for development & appraisal) are planned for H1 2025 and will be done in the Jasmine C, Jasmine D and Ban Yen areas (see map).

The company also wants to explore the Ratree area in H1 2025 (see map). This area could add between 3.4M and 41.9M bbls in reserves (mean of 19.4M). This is a much riskier opportunity but if successful it may be an entire new development by itself.

Finally, the company is also conducting a project in Jasmine that aims to reduce greenhouse gas emissions and opex by using a gas generator instead of a diesel one. If successful, it could be implemented in other oil fields.

Wassana (License G10/48)

Wassana was acquired through the KrisEnergy purchase. Valeura obtained an 89% interest in the oil field and 2P reserves of 2M bbls, which later turned out to be 6.5M bbls. A few months later, they acquired the remaining 11%. At the time of the acquisition the field was not operational because of a lack of a suitable FSO. They solved this quickly, leasing a FSO with a capacity of 460,000 bbls. They also own the MOPU in this facility.

The field operates under the Thai III terms with production rates of 4,200 bbls/d. The oil is typically sold at a $6/bbl discount to the brent price with opex of $36/bbl. The current 2P reserves of the asset are 12.9M bbls, which translates into 8.4 years of economic life at the current production rate.

Nevertheless, the exploration on this asset was successful and the company is expecting to increase production. The final investment decision (FID) on this asset should come in early Q2 2025, as per management guidance. It could expand the economic life of the field up to 2030 with up to 20 new wells. Previous exploration efforts were also successful with production increasing by 50% in Q1 2024 to about 5,000 bbls/d. Reserves have increased threefold after the acquisition.

It is also worth noting that the company now believes there is enough oil in the Niramai area (see map) to justify production there. This is not being considered in the current re-development project and the FID.

The Wassana field has also seen some complications, with two incidents occurring. First, the FSO moved from its intended position and operations were halted on July 7th 2023 as an act of caution. They were later restarted on Dec 8th 2023. The second incident came when a crack was discovered in the base of an oil rig. Operations were suspended and the rig was inspected. It turned out to be a superficial crack so it was quickly restored and operations were resumed.

Nong Yao (License G11/48)

The Nong Yao field is the largest and most profitable field for the company. Valeura’s 90% interest was acquired with Mubadala. At the time, reserves were 12.4M bbls (Valeura’s share) although the field had produced 20M bbls in 2021 (on a 100% basis). Production from Nong Yao was 8,100 bbls/d initially and later after the addition of Nong Yao C in Q3 it reached 11,400 bbls/d. They spent $56M preparing Nong Yao C for production. The field operates under the Thai III terms (roughly 8% royalty), with the oil sold roughly on par with brent and the operating costs being below $15/bbl for a few quarters now.

Reserves are still 12.4M, which equates to 3 years at current production rates. The current end of the economic life is 2028 but they expect to expand this to 2036 (license expiry) with the new Nong Yao D oil discoveries (see map). They are now planning appraisal drilling and expect the volumes to be enough to justify a development there.

Manora (License G1/48)

The Manora oil field was acquired with Mubadala. Valeura holds a 70% interest with current production of 2,400 bbls/d, which are sold on par with brent prices. The field operates under the Thai III terms and the royalty is around 8% with opex of $25/bbl. 2P reserves are 2.2M bbls, which puts the current field life ending in 2027.

Regarding exploration, when Valeura acquired the asset there was a decommissioning plan in place. However, it was put on hold when they discovered new oil in two wells, which may expand the field life from 2027 to 2030 (the license expires in 2033). Previous explorations had already pushed field life from 2022 to 2027. Additionally, in Q4 2024 they started a new 5 well drilling campaign that is expected to increase production rates in Q1 2025. This will solve bottlenecks in the Manora facility, allowing for increased production.

Exploration & Drill Rig

Regarding the drill rig, the company has leased a drill rig until August 2025. However, Valeura has recently stated that they have an “active drilling program throughout the year”, so it is possible that they have extended the lease. They also stated that their capex guidance for 2025 assumes one drilling rig for the full year. It is used for drilling the holes from which the oil is later extracted. The drilling can be for production/development or for appraisal/exploration.

The drill is now in the Manora field, where it will conduct a five-well program for development and appraisal, which should end in February 2025. After that, it will probably go to Jasmine for the exploration and development drilling. 80% of capex is directed towards drilling, which has had a historic success rate of 95%.

Rossukon Royalty

With the KrisEnergy acquisition, Valeura obtained a 43% interest in the Rossukon oil field. After discovering that it would take more than $100M to develop the asset, Valeura sold its stake for a payment of $5M payable at first oil (which offset a similar payment that Valeura owed) and a royalty of 4.65% on their 43% share, so 2% of gross production.

Thrace Basin

Valeura also holds a 83% interest in a gas project in the Thrace Basin in Turkey. They are looking for a suitable joint venture partner to restart their previous operations. They have been looking for a partner for the past 2 years and it is not expected that they will find one in the near term. The estimates of reserves for the field are 20T cubic feet of natural gas.

The license currently expires on June 27, 2025, but they intend to apply for extensions of the license.

Summary

Here is a summary of the oil assets in the portfolio and their operating conditions:

The portfolio as a whole produced about 26,100 bbls/d in Q4 2024. Oil is sold roughly on par with brent prices and with a royalty of 12%. Opex is around $27/bbl and adj. CFO is $29/bbl with capex under $15/bbl. Reserve replacement has also been high in recent years, with over 200% replacement in 2023 and expected replacement of over 100% for 2024.

Competitive Advantage

When it comes to competitive advantages, Valeura has two that are key to their future success. The first one is their management team and their ability and experience to find accretive deals, as demonstrated by their recent deals in Thailand. The other one is their ability to operate at very low costs, especially in the Nong Yao field. This gives Valeura the ability to finance exploration, increased production and M&A operations.

Financial Overview

Historical Performance

Before the acquisitions Valeura had $30M and was not producing any oil. After the acquisitions Valeura produced over 20,000 bbls/d and increased their net cash position significantly. At the end of 2023, their cash position was $150M with production of 21,000 bbls/d. At the end of 2024, production was above 26,000 bbls/d (for Q4) and the cash position was $260M, even after paying for all the exploration.

Balance Sheet

When it comes to the balance sheet, the net cash position stands out. It is $260M, which is roughly 50% of the market cap. Additionally, they hold about 0.65M bbls of oil in inventory, which are worth $50M at $80/bbl.

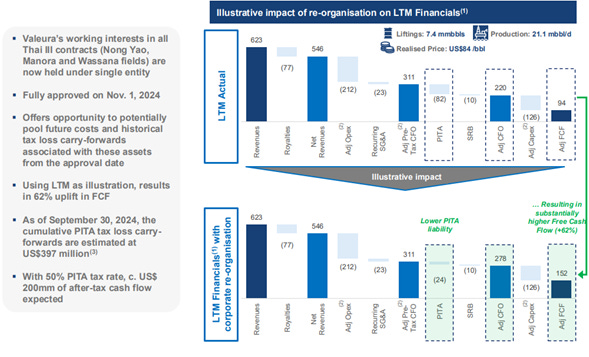

The other relevant line is the tax-loss carry-forwards that they have on the fields operated under the Thai III terms. With their first acquisition they also got $400M in tax-loss carry-forwards. Each of the fields was operated under its own company until Valeura decided to merge the Thai III fields under one company to take advantage of the previous tax losses. That way they can save up to $200M in taxes, mainly from their most profitable field, Nong Yao. This should increase cash flows significantly in the next few years. The merger was completed in November 2024. This is how it will affect cash flows, as explained in a company slide:

Profitability

Valeura’s profitability is very high mainly because of Nong Yao. It is the most profitable field because the assets used for production and storage are owned by Valeura rather than leased, coupled with easier to access oil. Here are some estimates of production and profitability for 2025 based on current production rates (at $80/bbl):

Growth Strategy

Guidance for 2025:

For 2025, management guidance is:

Note: opex of $26/bbl at midpoint.

At midpoint guidance and $80/bbl that would yield $330M for Valeura. After some other expenses (SRB, etc.) that could be $250M to $280M.

The guidance does not take into account the FID on Wassana, which could change exploration expenses and capex. Production will probably not be altered since it should take them more than a year to complete the expansion if approved.

Longer term and based on current assets, they think they can maintain production of 20,000 bbls/d to 25,000 bbls/d into the 2030s.

Growth Plan & Targets

The main target that management has set is producing 100,000 bbls/d by the end of 2026. They are 25% of the way there, but it is very possible that they reach their goal with acquisitions in the next two years. They had previously said (in 2020) that they would be producing 20,000 bbls/d by the end of 2024, which at the time seemed very far-fetched but they have achieved it with current production of 26,400 bbls/d.

To increase their current production, they are working to expand reserves in all of their assets. As explained before, they have multiple ongoing exploration projects. Some of them could expand reserves significantly as they explore new areas that have not had any oil extraction before.

Additionally, they are looking to acquire more oil fields in the region. In that regard, a comment from their last press release stands out: “The Company also seeks to grow its portfolio through mergers and acquisition within the Southeast Asia region and is actively evaluating several such opportunities”. They certainly have the financial muscle to make a big acquisition, possibly one above 50,000 bbls/d. The CEO recently said in an interview: “We can buy an asset of very significant magnitude here in Asia”. Whatever magnitude it ends up being, it can meaningfully increase Valeura’s FCF. The criteria for acquisitions is clear and simple: value accretive and cash generative currently or in the very short-term (“firm line of sight to cash generation”).

Capital Allocation

I believe that management’s capital allocation is top tier, as they have been able to create a ton of value for shareholders. When they sold their turkey assets the CEO stated: “I am pleased to announce the pending sale of our mature, conventional gas business as a way to strengthen our balance sheet and increase our cash to pursue higher-value growth opportunities. Our objective has been to maximise the value of these mature assets, and today’s monetisation agreement is a key step towards accomplishing that goal. We have re-tooled Valeura into a lean, shrewd, debt-free machine, focused on value growth”.

They turned $30M into $260M and production of $26,000 bbl/d in the span of 3 years. Besides exploration, they are now looking for more M&A opportunities and have started a buyback program. If they continue in this path, the future of the business is very promising.

Insiders & Shareholder Returns

Insider Ownership

Insiders as a whole own 6.6% of Valeura (7.13M shares) on a fully diluted basis (108M shares). Other important shareholders are Baillie Gifford with 11.8% and Thoresen Thai Agencies (TTA) with 15.75% (just over 17M shares). Baillie Gifford is a british investment firm while TTA is an oil & gas company operating in Thailand. TTA has recently been acquiring shares in Valeura. If they reach 20%, they will be forced to make an offer to acquire the rest of the company. Thoresen is an investment vehicle for one of the richest families in Thailand.

Most of the management team has previously worked for big oil companies (mainly Shell) and many of them entered Valeura through the acquisitions of KrisEnergy and Mubadala.

Dividends & Share Repurchases

Valeura does not pay a dividend, but it has recently started a buyback program. Under the program they can repurchase 7.4M shares until November 2025. They also set up an automatic share purchase plan to repurchase during blackout periods. From mid November to the end of the year they repurchased 0.35M shares, a rate of 2.6% annually.

It is also worth mentioning that they did issue some shares as a part of the expansion process. They raised CAD$10M that at CAD$2.54 are 3.94M shares. The proceeds were mainly used to finance pre-production operations in Wassana. They also issued 9.5M shares to acquire the remaining 15% of the SPV mentioned previously.

Risks

The risks for Valeura are:

Acquisition risk: although not likely in my view, they may acquire assets that turn out to be significantly less accretive than what they initially estimated, leading to bad returns for shareholders. Another possibility is that they can’t find any acquisition that is accretive for shareholders in any meaningful way simply because there are no opportunities available.

Operational risk: when operating oil rigs many unexpected things can happen such as oil spills, cracks, malfunctioning equipment, and a long etcetera. This can force the company to stop operations or be liable for damages like oil spills.

Oil Price exposure: a decrease in the oil price can damage profitability.

Nong Yao risk: most of the profits come from Nong Yao, so if they have to pause operations in Nong Yao profitability will fall significantly in the time the field is not producing.

Buyout: if Thoresen acquires 20% of the company they will be forced to issue a takeover offer for the entire company. They are now sitting at 15.75% but if they keep buying shares and Valeura continues with the repurchase program they may reach 20% within the year. That would be bad for the rest of shareholders since they will take for themselves the potential returns and cash flows.

Catalysts

There are several catalysts for the stock in the next few months. They are as follows:

2024 reserve report: Valeura will release the reserve report for 2024 in mid February 2025. Another year of reserve replacement of over 100% can be a good short-term catalyst.

Wassana Final Investment Decision: news of future increased production at Wassana can push the stock higher. The decision is expected to be published in April 2025.

M&A announcement: a new acquisition that is significantly accretive for shareholders is the biggest catalyst by far. When the last deal was announced the stock rose over 120% in a single day. Of course, it will not be that much this time but still it is the biggest catalyst for the stock for the next year.

Share buyback and Thoresen purchases: Valeura’s ongoing share buyback program and Thoresen’s continued purchases can keep pushing the price up in their short term.

Valeura also lists the exploration of the Ratree area in Jasmine and debottlenecking at Manora as short-term catalysts, both for mid Q2 2025. They will also release YE2024 financial results at the end of Q1 2025.

Valuation

Any valuation of Valeura will be inaccurate because you have to assign a value to many variables with high uncertainty. The value of Valeura ultimately depends on expansion of reserves (i.e. exploration success), production rates, oil prices, abandonment liabilities, and most importantly the acquisitions they make and the unit economics of the fields acquired.

Making a DCF based on current production rates and 2023 2P reserves (100% replacement for 2024) yields a NAV of CAD$7 per diluted share. The stock is trading at CAD$8, which means that the market is assigning a value of CAD$1 to all of Valuera’s potential future cash flows.

The analysts’ average target price is just under $10 and the ‘trading range from peer medians’ is $14, as stated by Valeura. That represents +25% and +75% upside respectively.

Valeura’s market cap is CAD$864M, which is $584M. Considering that they have $260M in cash, that leaves EV at $324M, or roughly 1.5 times FCF for 2025.

Note: the multiples are now 13.5, 1.16 and 1.55 respectively.

If valued at median multiples, the stock would be valued at around CAD$11. If they do reach 100,000 bbls/d of production and it reaches median valuation, the stock would be valued at over CAD$30.

Disclaimer

This article is not a financial advice. I am not a financial analyst. If you are going to invest do it under your own risk and after doing the appropriate due diligence.

Updates

In this section you can find the most relevant news and updates from the company since the thesis was published. They are arranged in chronological order:

No updates yet.