Achieve Life Sciences - $ACHV

A New Drug and a Possible Buyout

Note: this is the original thesis. You can access updates and new news about the company in the “Updates” section or at the end of this thesis, where you will find a link to all the updates.

Note: the post was written on March 25th when the stock was at $2.97/share. As of the publication of this post on April 9th the stock is at $2.14/share.

Business Model

Achieve Life Sciences (ALS) ACHV 0.00%↑ has developed a new plant-based drug for nicotine addiction called Cytisinicline, although the name will change soon. They have gotten the drug through all three phases of the FDA drug approval process and are now about to file their New Drug Application (NDA).

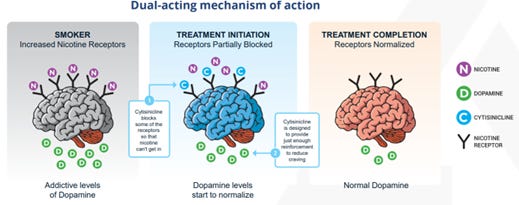

Once the patient starts smoking their nicotine levels start increasing and end up creating a dopamine addiction. Coupled with this process is a notable increase in nicotine receptors. What Cytisinicline does is blocking some of those receptors to start a chain reaction opposite of the chain reaction that created the nicotine addiction. Since some receptors are blocked, less nicotine gets released to the brain and gradually the dopamine levels and the number of nicotine receptors normalize.

The Drug

The previous smoking cessation drug was Chantix, which was launched by Pfizer in 2006. In 2021, Pfizer had to retire the drug from the market due to concerns about “N-nitroso-varenicline”, which was identified as a potential carcinogen. After this, other companies started selling the generic version of this drug, which is called varenicline. I will use Chantix meaning Chantix (the Pfizer drug) and varenicline (the generic drug) indistinctively since they are essentially the same.

Besides the carcinogen problem, Chantix came with a whole set of pretty significant side effects such as nausea, insomnia, abnormal dreams and headaches. By far the most significant one was nausea, which caused a significant portion of the patients to abandon the treatment.

Cytisinicline solves many of these problems. For starters, patients have significantly better odds of quitting if they use Cytisinicline. Here is a comparison between the currently available treatment options and Cytisinicline:

The odds ratio is about 5x, that is the patient has 5 times better odds of quitting if they take Cytisinicline compared to the placebo. That is twice the next best option, Chantix.

Furthermore, the side effects are significantly reduced with Cytisinicline, especially the nausea, which was the main reason for patients abandoning Chantix treatment. All the side effects are significantly reduced with Cytisinicline:

Cytisinicline has passed the studies of all three phases of the FDA drug approval process. All of these trials were conducted under the ORCA program, which stands for Ongoing Research of Cytisinicline for Addiction). There were two phase 3 studies, the ORCA-2 and ORCA-3 programs, which demonstrated the efficacy of the drug in both their 6-week and 12-week treatment plans. Here is the evolution of quit rates for the ORCA-2 and ORCA-3:

After those trials were completed, the company expected to submit their NDA but the FDA asked for additional studies to asses the long-term impact of the drug. This is probably because of the issues that Chantix had in the past and the FDA not wanting to take any risks, although they are completely different drugs. Nevertheless, they were forced to conduct a 6-month and 12-month study (ORCA-OL trial) to assess the long-term impact of the drug. The results for the first six months were released and no problems were identified. After the completion of the 6-month study they now have all they need for the NDA application, which is expected to be filed in Q2 2025. The 12-month study will continue until the end of June 2025, although the 6-month study is enough to satisfy the long-term safety requirements of the FDA.

The company is also working towards getting the drug approved for e-cigarette users, since the current trials only cover conventional smoking. In this regard, they have completed the ORCA-V1 trial, which was a phase 2 trial focused on evaluating the safety and effectiveness of the drug for users of e-cigarettes. The trial showed successful results and the company met with the FDA to design the phase 3 trial, which will be called ORCA-V2. The trial is expected to begin in Q3 2025 and it should last 24 weeks (12 weeks for treatment and 12 for the follow-up period).

Achieve is also working on the commercial name for Cytisinicline, which is already pre-approved by the FDA, but it has not been disclosed yet.

Finally, it is also worth noting that a different version of Cytisinicline is being sold in Eastern Europe since the 1960s under the brand name Tabex.

Timeline

Achieve should file its NDA for Cytisinicline in Q2 2025. After that, the NDA should be accepted and reviewed by the FDA and finally they should grant final approval. The drug has breakthrough designation, which means faster approval times from the FDA (aka priority review). The FDA has 60 days to accept the NDA (from submission) and then another 6 months for review. They are expecting approval in H1 2026 and product launch in H2 2026. However, this is not likely as I will explain later.

Here is the full timeline of company events, including FDA events and trials:

Market

The number of adults in the US who smoke or vape is 40M, with 29M adult smokers and 11M adult vapers. Every year roughly 15.4M smokers and 6M vapers try to quit. That is 53% and 54% respectively. However, only 9% of adults successfully quit, as per CDC data.

About 36% use recipe and over-the-counter treatments each year. Particularly, only 10% of those who try to quit take prescription medications. This, coupled with the fact that there have been no new FDA-approved options in the last 20 years provides Achieve with a very interesting market opportunity.

Regarding the number of patients that might use Cytisinicline, it is fairly easy to estimate. Lupin, a provider of the generic version of Chantix, estimated about $430M annual sales in the US. According to a research study (https://doi.org/10.1161/STROKEAHA.122.040356), “We estimated the cost of varenicline to be $473 for a 3-month supply of medication, which is the standard course of treatment”. That yields 910,000 prescriptions per year. Achieve also states that Chantix peaked at 2.8M recipes, which divided by the three dosages needed means that about 933,000 patients received it, which is a very similar number. However, Pfizer was able to sell $1.1B and $919M in 2019 and 2020 respectively on a similar number of prescriptions, meaning they had a significantly higher price, almost $1,500 per treatment ($500/month over the three months).

Competitive Advantage

For Achieve Life Sciences the competitive advantage is pretty straightforward since they hold a patent on the drug plus a few other patents on dosing and formulations. Additionally, management has stated that it takes a while to grow the plant from which the drug is elaborated. Specifically, the tree is called Cytisus laburnum and it takes between 3 and 5 years for it to grow so that it can produce enough cytisine.

Achieve lists their patents and expiration dates in a slide in their investor presentation:

Financial Overview

Revenue and Profitability Estimates

As previously explained, the market for nicotine cessation drugs for cigarette users has about 900,000 patients each year based on Chantix’s sales (assuming they had a 100% market share, which they didn’t). For a broader perspective, about 10% of those who try to quit do so via medication, so about 1.54M patients. Cytisinicline is clearly a better drug than Chantix (or its generic version), so it has the potential to capture a significant part of the market, perhaps even more than Chantix.

However, I will assume that they get 50% of Chantix’s patients (450k patients) if they use a price of $350 per month, so $1,050 for the entire treatment. I believe this is a conservative number considering that Pfizer was selling Chantix at $500 per month ($1,500 for the entire treatment) in 2019 for a worse medication. That would be roughly $475M in annual sales. I think that they convert 25% of that into FCF easily, which would leave about $120M in annual FCF.

Another more optimistic scenario, although very possible in my opinion, is that they sell to 750k patients at a total price of $1,200 per treatment and with margins closer to 35%. That would be $315M in annual FCF and that is not even accounting for the vaper users.

They have also stated that they want to fund the commercialization of Cytisinicline by themselves. For this they would need to hire sales representatives and incur in many other expenses to promote the drug. The company has stated that out of the 460,000 doctors that write prescriptions for this type of drug, only 10% of them write 60% of the prescriptions. The annual cost of hiring a sales representative is $125,000 per year, according to a research article (https://doi.org/10.1016/j.eswa.2007.01.037). Assuming 250 working days and two visits per doctor you would need 184 sales representatives, for which the cost would be $23M. Add digital campaigns, medical conferences, booths and speaker programs, among others, and you can easy get to $50M per year. Say it takes two years to ramp up and you need $100M to launch the drug, plus the 39 months until the end of the ramp up period (15 months until H2 2026 plus the 24 months of ramp up). That adds $117M in costs for a total of $217M (see monthly cash burn below).

Financial Position

Achieve is a pre-revenue company so they are dependent on external financing and cash balances. Their last financing round was in February 2024, from which they received $60M from several biopharma funds. They issued just over 13M shares at $4.585 per share. They also issued 13M warrants with an exercise price of $4.906 per share, which will provide $64.2M upon exercise. The warrants are exercisable immediately and expire on August 2027 or 30 days after NDA acceptance (yes, acceptance not approval). This poses an interesting situation for the warrant owners since the exercise price of the warrants is $4.9 while the current stock price is $2.97.

The current cash burn is approximately $35.1M annually (roughly $3M per month), which is the negative $29.77M cash from operations but without accounting for the $5.325M from stock-based compensation. At the end of 2024, Achieve had a net cash position of $24.4M, which can cover 8 months of expenses. Achieve will run out of cash by August 2025.

Share Count

With the February 2024 financing, the company went from 21.17M shares to 34.25M, which is a dilution of 62%. The new owners thus controlled 13.1M shares or 38% of the company post-financing. However, they also received another 13.1M shares in warrants. If exercised that would add another 13.1M to the share count. Taking into account other warrants, stock options and RSUs, the total diluted number of shares is 55.77M. So, if the warrants were exercised the holders of those warrants would own 47% of the company. If they expire worthless, they would own 30.7%.

The company has 2,139,414 stock options and 1,283,750 RSUs outstanding. The warrants are as follows:

The total outstanding warrants are 17,664,255.

Valuation

If you use a p/fcf of x10 the value for the company would be between $1.2B and $3.2B based on the previous estimates of FCF. Say that the company ends up being bought after the financing round for $1.2B and during said financing round they want to raise ~$170M (most of their estimated financing needs). That would be a 100% dilution from the current fully diluted market cap of $170M and would leave the total number of shares at under 120M. Under those conditions the buyout price is $10/share, 3x the current price.

It is hard to estimate what a buyout price would be or how much the company ends up selling but there is enough margin of safety to justify an investment at $3/share, especially considering that some funds who control 30%-47% of the company bought at $4.5/share and at the time knew that they may have to add the extra $64M from the warrants.

There are many possibilities for the future of the company but ultimately this is what is known:

Achieve runs out of money in August 2025.

They would need to dilute massively (>100%) to get the funding needed to commercialize (or get into debt but that is more unlikely).

The product has the potential to generate significant profits once it is selling and scaled up.

Investors put $60M at $4.5/share and own 30% of Achieve.

Investors also have warrants that could put their ownership at 47% but would require them to invest another $64M at $4.9/share.

Those warrants expire after the FDA accepts the NDA (30th September at the latest).

The stock is currently at $3, so the investors controlling 30% won’t allow a sell below $5/share. They won’t allow diluting either if they are not the ones receiving the new shares at $3. (Because that would dilute them, when they can instead exercise their warrants, provide the company with cash and then pursue a sale at above $5/share).

Furthermore, the future of the company and retail investors depends on:

Whether the warrants are exercised or not. They could also renegotiate the exercise price and exercise them at a new, lower, price.

The terms of any other possible financing and the ultimate goal of that financing (just surviving until FDA approval and buyout or commercialization).

The timing of the buyout (if any), especially whether or not it happens before FDA approval or refinancing. I expect that if there is a buyout offer it would be from a large pharma company.

The potential catalysts are basically the sale of the company, a successful refinancing with a clear action plan or the presentation, acceptance and approval of the NDA.

This leaves a relatively complex setup of a game theory situation where many different players are involved and the decisions they take or might take influence other players’ decisions. Ultimately there is no way to know what will happen, although I think that the most likely outcome is that the warrant holders exercise them and eventually pursue a sale of the entire company.

Insiders & Shareholder

Unfortunately, insiders own very little stock out right, but they have about 3.4M in RSUs and stock options. They have also recently purchased some shares:

The CEO had some shares already and he now owns 60,876 shares, about $180,000. The main shareholders are:

Risks

The risks are:

Dilution risk: the current shareholders get massively diluted (more than the estimated 100%) and the returns get greatly damaged. I think that is only possible if the stock keeps on falling and the investors who own 30% manage to be on the next financing at a much lower price. If they are not in the next financing, they are not incentivized to let others put the money in, they get diluted.

Financing: they may not be able to get the additional capital that they need to survive until FDA approval. I do not think this is likely since investors have put a lot of money into Achieve under much less certain circumstances than today.

FDA approval: this should not be a problem since all the trials have gone well and the drug has been sold in Eastern Europe since the 1960s. Any potential negative side effects should have been spotted by now.

Other nicotine addiction drugs: if another competitor manages to get another similar drug through FDA approval it could damage potential sales. I think this is highly unlikely since Cytisinicline is the first nicotine cessation drug in 20 years.

Disclaimer

This article is not a financial advice. I am not a financial analyst. If you are going to invest do it under your own risk and after doing the appropriate due diligence.

Updates

In this section you can find the most relevant news and updates from the company since the thesis was published. They are arranged in chronological order:

No updates yet.

Any view on the offering here?

Interesting thesis, looking forward to seeing how this investment plays out.